($) TSMC: Where and How Will It Raise Prices

Before we get into today’s premium member post, a quick update on last year’s fund performance. My 2023 annual performance was examined and verified by a third-party independent accounting firm (Spicer Jeffries). The result is 170.13%, net of all management and performance fees. The report is available upon request for any capital allocator interested in reading the details. Now, onto today’s post.

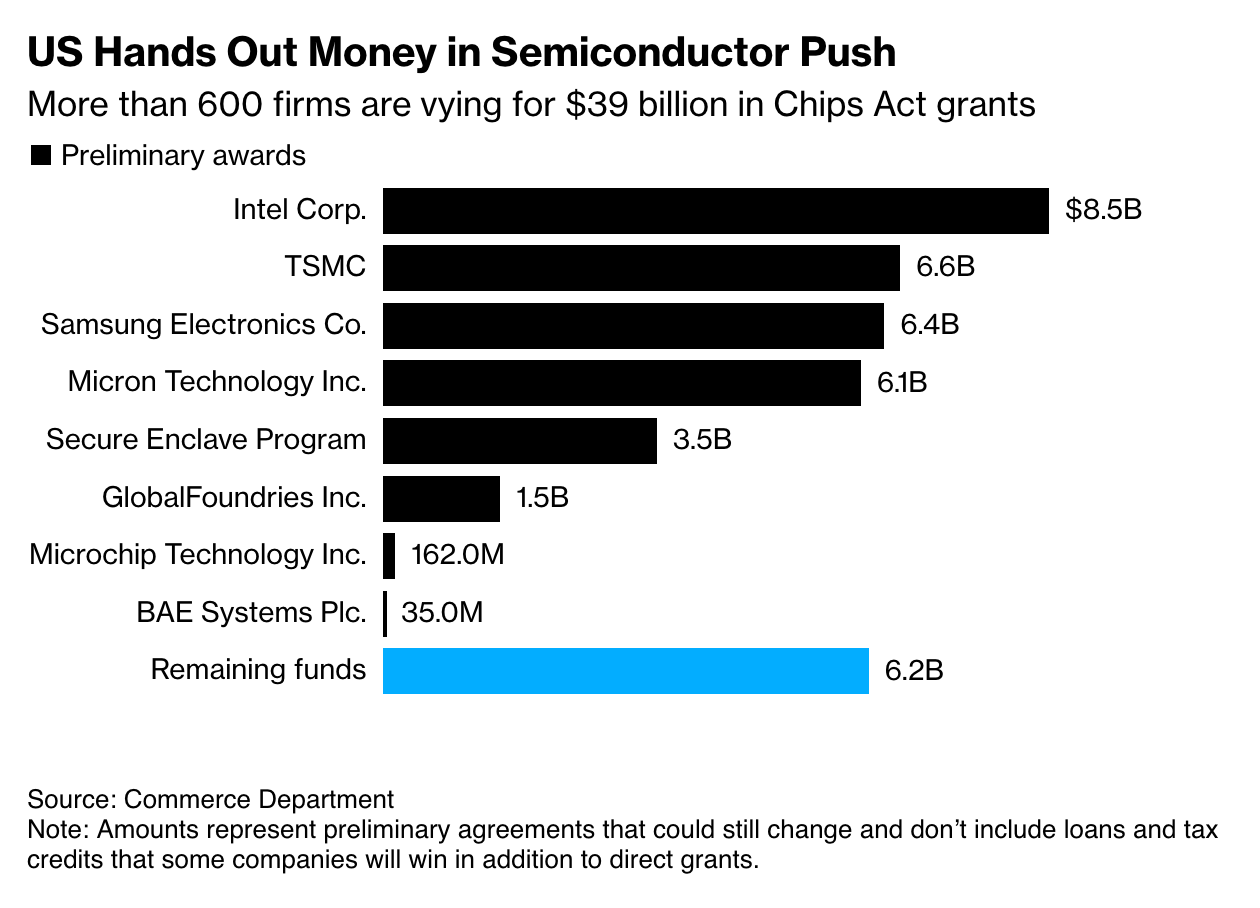

Most of the CHIPS Act subsidies have (finally) been (preliminarily) allocated.

Out of the pot, and out of the companies’ whose fabs and capabilities actually matter in the industry, Intel got $8.5 billion, TSMC got $6.6 billion, Samsung got $6.4 billion, and Micron got $6.1 billion. That is 70% of the total pie of $39 billion that’s made available by the CHIPS Act. There is $6.2 billion left in the pot, and I expect remaining American companies, like Texas Instruments, to receive some of what’s left.

The allocation of these subsidies alone took a surprisingly herculean effort by the Commerce Department, which had to stand up a CHIPS program office from scratch and hire hundreds of staffers to receive, vet, and decide on all the applications. As America’s first go at a major industry policy in a long while, reaching this milestone deserves some celebration and relief.

Sadly, this celebration can’t last long because it is the easy part of onshoring advanced semiconductor manufacturing onto US soil. As Morris Chang likes to say, this is just the “end of the beginning.” Among all the companies that have received subsidies, only TSMC really matters, if we focus on the “advanced” part of advanced semiconductor manufacturing. When Commerce Secretary Gina Raimondo boasted about how the US has the “most sophisticated semiconductors in the world” on 60 Minutes, and Lesley Stahl pushed her by retorting “you mean Taiwan,” the Biden cabinet member begrudgingly responded, “Fair...”

Even with these subsidies, there is a common assumption that TSMC’s fabs outside of Taiwan will be less profitable due to the various foreseen and unforeseen costs of building “geopolitical redundancies.” Yet, TSMC has maintained and reiterated its longstanding financial goal of delivering 53% gross margin or higher. So the only way it could do so, amidst the obvious specter of higher cost, is raising prices.

With this first stage of CHIPS Act implementation behind us, we finally got some clues from TSMC’s most recent earnings call on the “where and how” of its plans to raise prices.